The Internet, Retail Investing, and Financial Freedom

Retail investing has changed some peoples’ bank account balances, but not the world.

This is the first guest-written piece for the IDW Feed, by fellow Substacker Unraveling Economics!

A new generation of Internet-savvy financial advisers and bloggers has come of age over the last few years. They contend that with the rise of retail investing and the wealth of investing knowledge available online, regular people have a historically unique opportunity to earn financial freedom independent of the typical intermediaries. It’s a vision that promises people a sense of agency and empowerment during a time when so many feel that they exert little control in the workplace or over the economy generally. Through intelligent investment, people are promised financial independence, an escape from the rule of elites, and even a more democratized society through the dispersion of ownership.

Let’s begin with the obvious: the Internet has revolutionized the process of investing. Payments processors like PayPal and Zelle have rendered simple the online transfer of funds. And online investment platforms like Robinhood have made investing accessible for everyone; no longer does one need to rely on the local banker or financial adviser for investing. The result has been a meteoric rise in retail investing, which began in the mid-2000s, but enjoyed a massive resurgence in 2020 when Covid-19 stimulus checks provided Americans a sudden surge of liquidity and the Gamestop phenomenon—along with surges in penny stocks and other securities highly favored by retail investors—instilled in them a belief that high returns could be reaped rapidly. According to Charles Schwab, 15% of all investors in the US stock market made their start in 2020.

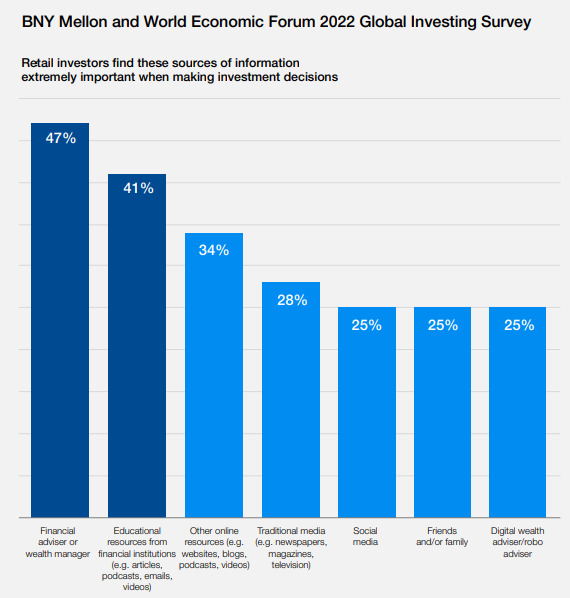

These new investors are particularly reliant on the Internet for information. According to the 2022 Global Investing Survey conducted by BNY Mellon and the World Economic Forum, over a third of retail investors deem miscellaneous online sources “extremely important” for investing information, while one-quarter say the same about social media.

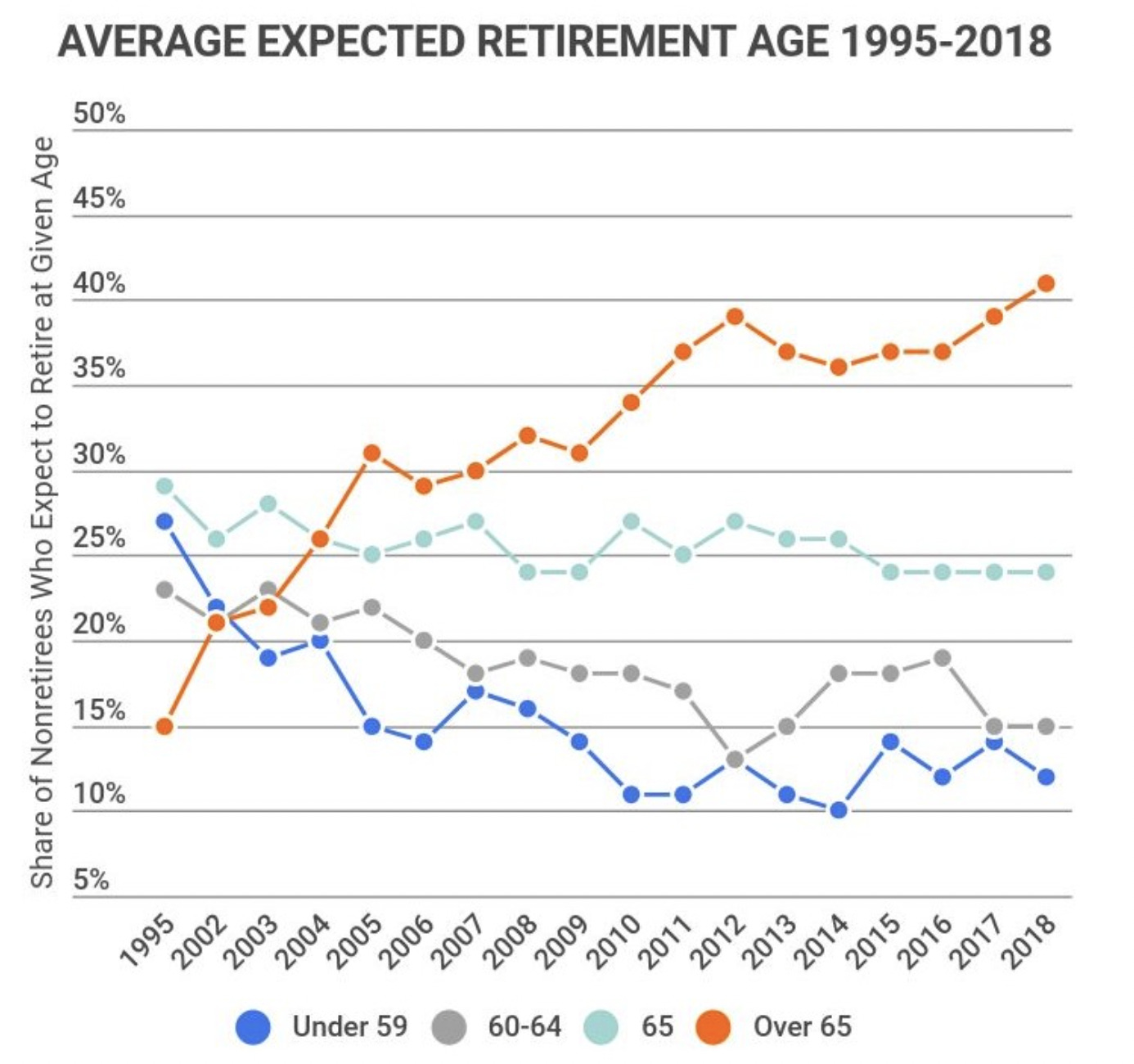

Despite these massive changes in how financial markets operate and the people operating in them, much remains the same. Incomes were not significantly boosted by investment returns after the end of the pandemic. The average retirement age for Americans is still climbing, though a slightly greater portion of Americans are planning to retire a few years sooner. And investment returns have not changed substantially, though they have been much more volatile in the years surrounding the pandemic.

However, one might not expect these developments to have large, easily-observable aggregate impacts. After all, averages don’t well capture the success of today’s Horatio Algers and can be confounded by all sorts of unmeasured factors. When studied at a more granular level, the appeal of retail investing remains limited. Studies of retail investors suggest that the vast majority of them (sometimes a share as high as 97%) lose money. There are a few reasons for this. First, beating the market is simply difficult. Few experts are able to accomplish it, and over several years passive investment funds almost always manage to outperform active funds. Second, retail traders are more likely to buy into online “hype,” herding their cash into one “pump-and-dump” after another. Yes, those clever enough to cash out at the stock’s peak might experience temporary gains, but few are talented enough to win repeatedly. As explained by one study of retail investor performance:

[T]he top 0.5% of stocks bought by Robinhood each day experience return reversals on average of approximately 5% over the next month whereas the more extreme herding events have reversals of approximately 9%.

They conclude: “Large increases in Robinhood users are often accompanied by large price spikes and are followed by reliably negative returns.”

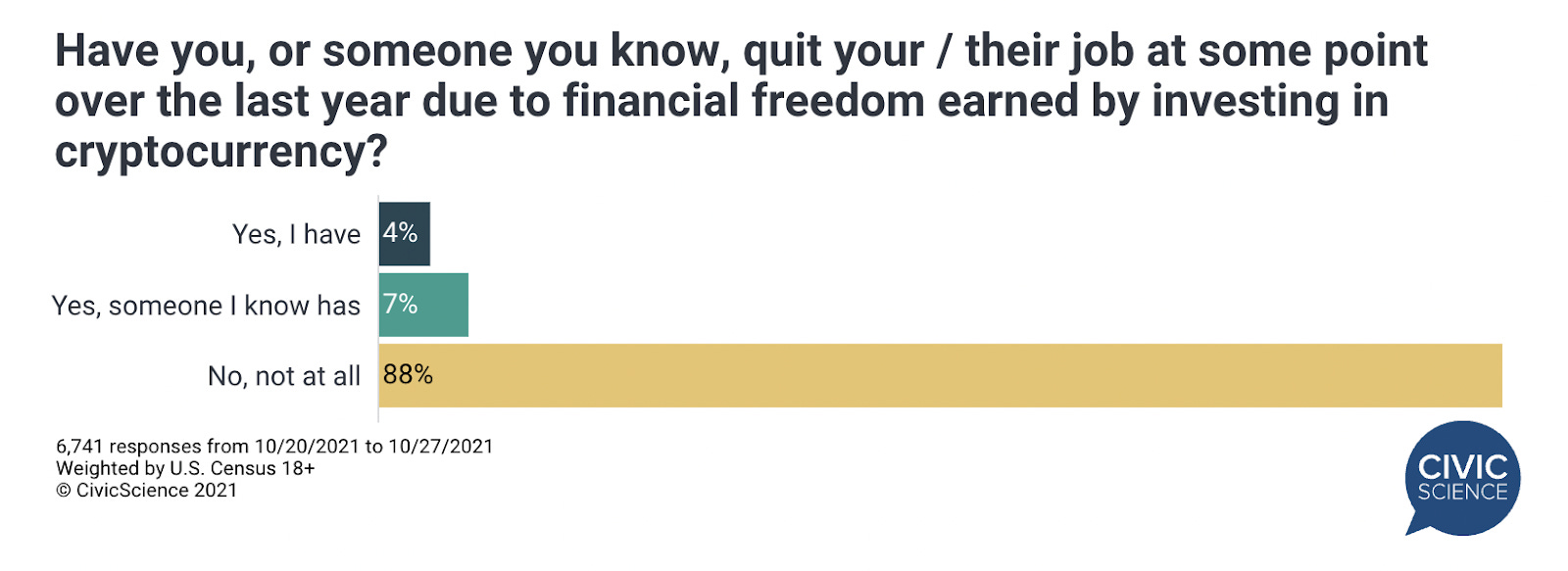

But at least investors on Robinhood are primarily trading stocks, regulated securities issued by firms with real assets. The Internet has also facilitated the growth of a variety of less-reputable assets designed to milk gullible traders of their cash. For a brief period the news media was incredulous about all of the cryptocurrency millionaires created in 2020. One poll, heavily covered in financial media, even claimed to find that 11% of Americans had or knew someone who had quit their job thanks to cryptocurrency profits. (One wonders if many people only knew of such individuals through popular news stories.) These assets have lost much of their original popularity thanks to the rapid fall of Bitcoin, the passing fad of NFTs, and the implosion of FTX, and though institutional investors have gotten more involved in them as a means of diversifying their portfolios, they remain largely a money pit for well-meaning but unthoughtful amateur traders.

And that brings us to our next point. The Internet has allowed the investing information available to the everyday person to grow exponentially, but that doesn’t mean that most of that information constitutes sound advice. The Internet has few mechanisms to help sort good advice from bad, or to determine whose success was a product of luck as opposed to actual market insight. Given the average returns of retail investors that we just discussed, the most optimal move for most of them is to follow the sort of simple advice that one can get offline: save a portion of your income; invest in passive funds with a level of risk appropriate to your stage of life and with low fees; and don’t panic-sell during recessions.

This isn’t exactly groundbreaking stuff. For years, Charlie Munger has explained that "The big money is not in the buying and the selling but in the waiting." But nobody wants financial freedom the boring way, by investing 5% of your paycheck in a passive fund with an average annual return of 6% for 35 years. They want the sudden freedom enjoyed by crypto-millionaires and the few individuals who hit big in retail investing. A small minority will achieve this, but because everyone wants to think they have the special talent —that Wolf of Wall Street-like instinct for spotting the next big thing— an unreasonable amount of people will continue trying, fueling asset bubbles and depleting their savings.

What about the broader social impacts of retail investing? Aside from a lot of chatter about a “retail investor revolution,” there are few. Sure, new trading platforms have spawned to cater to young retail investors, promising lower fees and commissions. Social media panics can help determine a stock’s trajectory in the short-term. And a greater share of the total market capitalization of the stock market is now directly in the hands of retail investors, having jumped from 15% to 21% since 2019. But this change in ownership has done little to change how firms actually behave. It’s been over ninety years since Gardiner and Means first outlined the great division between ownership and control in the modern industrial economy; ownership in the form of stocks does not necessarily grant holders the control that used to customarily accompany ownership. That control is still retained by corporate boards of directors and a small collection of institutional investors, particularly the commercial banks, pension funds, and asset management firms that control the large majority of outstanding shares.

The closest retail investors ever came to wielding any real power was during the Gamestop debacle of 2020, in which an army of collusive Redditors temporarily got the better of institutional investors by employing a short squeeze against those who bet against the success of Gamestop. But the retail investors’ success was only temporary, and without stimulus, likely unrepeatable. As Spencer Jakab, author of the most prominent book on the Gamestop debacle, The Revolution That Wasn’t, put it:

Sure, the situation got out of hand and the little guys may have shocked the establishment, but did they really stage a revolution? Far from it. Retail traders have a traditional place in Wall Street’s food chain, and that hasn’t changed once the dust cleared and the profits and losses were added up.

Thus far, a growing collection of ownership and a sudden revolutionary moment have both failed to help retail investors even slightly supplant the power of the financial establishment. To defeat that establishment, political organization and action would be required, and a bunch of atomized investors have little capacity to carry that out. They have no lobbyists, no politicians, nobody’s savings to invest but their own, and no real capacity to privately coordinate and strategize, aside from participation in mostly-public online forums.

For a select few, retail investing will prove life-changing, allowing them to withdraw from work and retire to a comfortable plot of land free from the traditional economic worries that compel so many of us to work. But, as Joni Dean famously put it, “Goldman Sachs doesn’t care if you raise chickens.” A few newly-wealthy individuals choosing to withdraw from society does not inhibit the power or influence of the financial establishment. If you want to try your hand at retail investing, be aware that your chances at success are long, and that if you succeed you may significantly change your life, but not necessarily the world. Your financial freedom can empower you to commit your time to all sorts of socially-productive activities, but personal enrichment itself should not be confused with revolutionary practice.

| A guest post by

|