Like this post? See the main page for the rest of the Financial Freedom series!

Arbor Realty Trust is a lender that primarily gives short-term loans to real estate developers in the multi-family housing market. Thus it is considered a mortgage real estate investment trust (mREIT).

History

Origins (1983 - 2007)

The company was founded in 1983, with a business of issuing mortgages to homeowners. The name “Arbor” is tied to their practice of planting a new tree with every new home that was bought with their mortgages. In the 90s, it spawned a commercial lending operation and sold its residential mortgage business to Bank of America in 1995.

By 2003 they expanded into loans for multifamily rentals and adopted the current name of Arbor Realty Trust. In 2004, they launched their IPO under the current shares of ABR.

Great Recession and Recovery (2008 - 2019)

The disruption of financial markets by the 2008 Financial Crisis negatively impacted the company, depriving them of capital to raise to issue more loans, while the housing crisis made it harder for their customers to leverage their real estate to take out new loans.

Their balance sheet took a hit with several loans that would thus never be paid, but the company was financially healthy enough that it did not get wiped out and continued to have positive operating cash flows in spite of this. The annual dividend, which had peaked at $2.57 in 2006, was reduced to $2.10 in 2008 and completely eliminated until 2012, once originations and earnings were able to pick up again.

In 2016, the company merged with its asset manager and, in so doing, acquired its agency origination platform. Since then, shareholders of ABR derive earnings from not only from interest income but on the loanbook but also on the servicing fees for these agency loans.

Recent Years (2020 - Present)

The onset of COVID strained most mREITs and required dividend cuts or eliminations, but this was not so for Arbor. In fact, during each quarter of 2020, they increased their quarterly dividend, despite fears of the market.

While other mREITs lacked access to capital during the pandemic, Arbor was able to raise $233 million through debt and equity offerings and continued to originate loans with minimal delinquencies.

2021, 2022, and 2023 both followed the trend of dividend increases, in spite of other challenges posed by leftover effects of the pandemic, inflation, and the War in Ukraine.

The rise of interest rates actually helped Arbor, whose portfolio is mostly floating rate loans. As Arbor’s own liabilities primarily consist of fixed-rate debt, this caused their net interest income to increase, making 2022 a very profitable year for the company.

Current Strategy

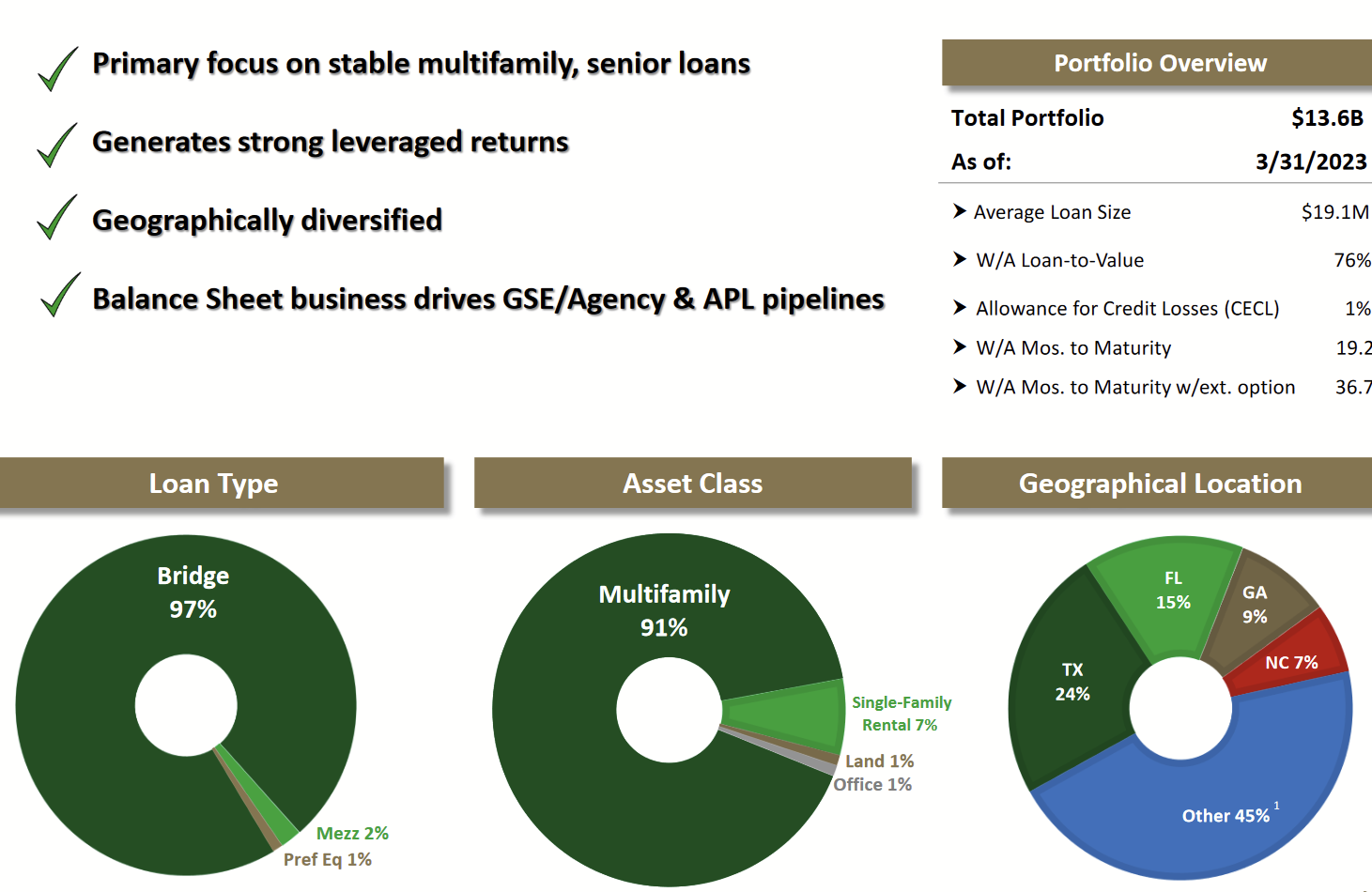

The company mainly prefers to operate in its own loan origination, called the Structured Business, and the Agency Business, which originates loans for sale to Fannie Mae and Freddie Mac.

Structured Business

Most of the loans that Arbor issues directly are bridge loans in the multifamily rental sector, but other types of loan products exist on their origination platform. Bridge loans are typically short-term in nature, lasting about a year, to provide real estate buyers the capital necessary to buy a property quickly.

Profits from the Structured Business come from the spread between interest payments received on these loans and the interest they pay on their own loans.

Agency Business

These are loans which Arbor originates on behalf of U.S. agencies such as Fannie Mae and Freddie Mac. Since acquiring it in 2016, this portfolio has steadily been growing.

Cash Flows

Unlike most of mREITs, ABR has a more diversified, adaptable system of cash flow to make its distributable earnings more consistent across multiple environments.

For investors seeking its dividend, this is an important feature of Arbor.

Risks

Let’s look at the individual factors that could risk the dividend.

Default

Arbor seems to have improved its loanbook since 2008 by expanding into other regions and having more regional diversity for those cash flows. A major disruption like the financial crisis could occur again, and even its conservatives loans would face risk of default. While Arbor has not faced deliquencies like those of 2008 and has managed to sustain its dividend, it’s unclear how much Arbor’s evolution in its practices and business model would ensure its continued dividend.

Stagnation

Even if Arbor’s loans holds out, a disaster that disrupts capital markets would make it harder for them to raise capital for investment or for their customers to raise capital to purchase real estate. REITs like Arbor distribute most of their earnings and therefore have little capital retained for newer originations. While business could eventually pick up again, a lull period could result until capital markets improve.

Agency Business

While originating loans for agency securities give them steady cash flow from the servicing fees, Arbor is temporarily liable for unpaid principal and interest on delinquent loans for up to four months. The agencies will ultmately reimburse them, but a concentration of unexpected delinquencies in their Agency portfolio could cause a liquidity crisis.

Dilution

Since REITs distribute most of their earnings, they often issue new shares of their companies to raise capital for growth. Over the last decade, Arbor’s dividend growth and capital appreciation have exceeded their rate of share dilution, but this is not guranteed. Under stress, Arbor may be forced to issue equity to raise cash at an unpleasant rate of return for current holders.

Conclusion

These facts are for readers to use. Whether shares of ABR are a favorable investment is for them to decide.

Like this post? See the main page for the rest of the Financial Freedom series!